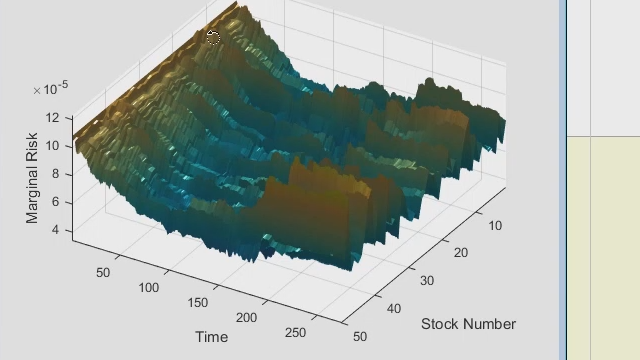

In this webinar you will learn how to use MATLAB for portfolio construction. Through examples and demonstrations, attendees will see how they can use MATLAB and the Optimization Toolbox to construct portfolios using techniques beyond the classical risk/reward or expected shortfall methodologies.

The presentation will highlight some aspects of Smart Beta strategies and also show how to build a simple yet scalable stock selection model for equity portfolio construction.

Attendees will learn how to:

- Construct portfolios using custom risk measures, such as Risk Parity or Drawdown

- 建立基础和价格驱动因素

- Construct and backtest a portfolio using stock selection criteria

- Build desktop tools that allow a Portfolio Manager to quickly test and optimize a strategy

Dan Owen is Industry Manager for Financial Applications for the APAC region. Dan has worked at MathWorks for over 12 years in Consulting and also as an Applications Engineer, always focusing on Financial Services. He has also worked as a Director of Systematic Trading at Dresdner Kleinwort and also within a Quant Technology group at Fidelity International. He holds a BSc and a PhD in Applied Mathematics from the University of Birmingham in the United Kingdom.