Cointegration and Pairs Trading with Econometrics Toolbox

William Mueller, MathWorks

Stuart Kozola, MathWorks

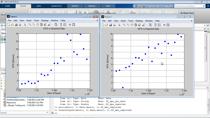

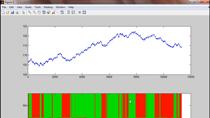

Learn how Econometrics Toolbox can be used to create better time-series models and forecasts. In this webinar, we will introduce new capabilities with the R2011a release of Econometrics Toolbox that include cointegration tests and vector-error-correcting (VEC).

Short examples will be used to illustrate the new features followed with an applied case study in pairs trading.

关于演示者:

Stuart Kozola is a product manager at MathWorks and focuses on MATLAB® and add-on products for computational finance.

William Mueller is a developer at MathWorks and focuses on computational finance products, including Econometrics Toolbox™.

View example code from this webinar here:

//www.tatmou.com/matlabcentral/fileexchange/31060-cointegration-and-pairs-trading-with-econometrics-toolbox

Related Videos and Webinars

选择a Web Site

Choose a web site to get translated content where available and see local events and offers. Based on your location, we recommend that you select:.

选择web siteYou can also select a web site from the following list:

Americas

- América拉丁(Español)

- Canada(英语)

- United States(英语)