A credit scoring model is a mathematical model used to estimate the probability of default, which is the probability that customers may trigger a credit event (i.e. bankruptcy, obligation default, failure to pay, and cross-default events). In a credit scoring model, the probability of default is normally presented in the form of a credit score. The higher score refers to a lower probability of default.

Although there are a number of common credit factors in credit scoring models, different types of loans may involve different credit factors specific to the loan characteristics. For example, the credit factors for a credit card loan may include payment history, age, number of account, and credit card utilization; the credit factors for a mortgage loan may include down payment, job history, and loan size.

Accurate and predictive credit scoring models help maximize the risk-adjusted return of a financial institution. However, markets and consumer behavior can change rapidly during economic cycles, such as recessions or expansions. For this reason, risk managers or credit analysts need not only to create the models, but also quickly adjust and validate them. Techniques used to create and validate credit scoring models include:

- Logistic regression andlinear regression

- Machine learningandpredictive analytics

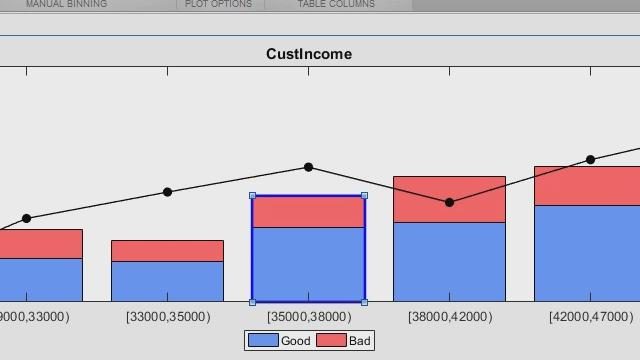

- Binning algorithm (i.e., monotone, equal frequency, and equal width)

- 累积准确性概要(CAP)

- Receiver Operating Characteristic (ROC)

- Kolmogorov-Smirnov (K-S) statistic

For more information on credit scoring models, seeMATLAB®,Financial Toolbox™, and风险管理ment Toolbox™.