MATLAB for Quantitative Finance and Risk Management

Import data, develop algorithms, debug code, scale up processing power, and more.

In just a few lines of MATLAB®code, you can prototype and validate computational finance models, accelerate those models using parallel processing, and put them directly into production.

Leading institutions use MATLAB to determine interest rates, perform stress tests, manage multi-billion dollar portfolios, and trade complex instruments in less than a second.

- MATLAB is fast: Run risk and portfolio analytics prototypes up to 120x faster than in R,100xfaster than in Excel/VBA, andup to 64xfaster than Python.

- MATLAB automatically generates documentation for model review and regulatory approval.

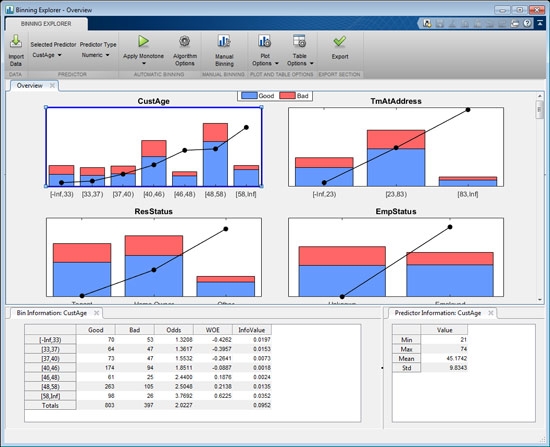

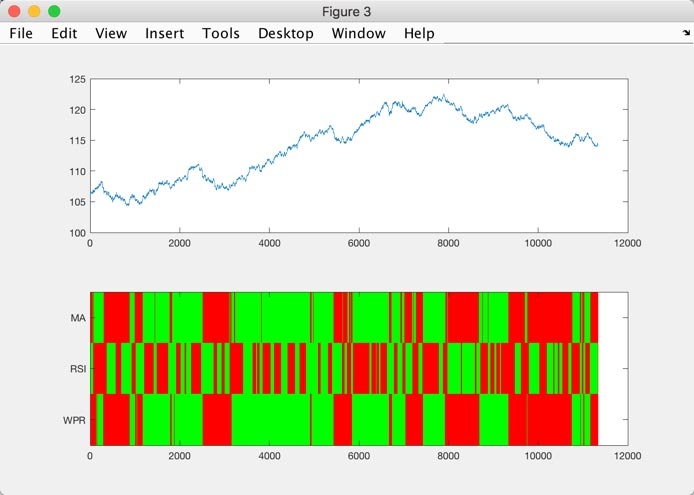

- Analysts use prebuilt apps and tools tovisualizeintermediate results anddebugmodels.

- IT groups can deployIP protected models directly todesktop and web applicationssuch as Excel, Tableau, Java, C++, and Python.

- MATLAB includes an interface for importing historical and real-time market data from free and paid sources includingBloomberg,Refinitiv,FactSet, FRED,andTwitter.

- MATLAB handles big and streaming data from traditional and alternative data sources.

“MATLAB enabled us to concentrate on our core competencies as investment professionals and deploy a quantitative risk management and portfolio optimization dashboard that has added value from day one across our team.”

Mathew John and Jason Liddle, SMMI

Free White Paper

Effective Model Risk Management with MATLAB

24 technical talks on new capabilities

in MATLAB and Simulink

Investment Management

- Build and evolve dashboards for portfolio managers, with intraday risk reporting, valuation, and trade execution capabilities.

- Use prebuilt tools for performing portfolio optimization using mean-variance, mean absolute deviation (MAD), conditional value-at-risk (CVaR), andBlack-Litterman methods.

- Measure investment performance using risk-adjusted alphas, tracking errors, maximum drawdowns, and the Sharpe ratio.

Explore Products

Risk Management

- Automate, augment, and provide executable reporting throughout the risk model lifecycle. Take models through model validation, model review, implementation, and regulatory approval in just three months.

- Build risk management systems or stress testing infrastructure for CCAR, DFAST, Basel III, and Solvency II.

- 使用模型和函数来量化风险(e.g., market, credit, and operational risks), validate the models using VaR and expected shortfall backtesting, and supplement the traditional methods with machine learning algorithms and text analytics.

Explore Customer Success Stories:

Financial Forecasting and Modeling

- Use point-and click apps to fit time-series data with econometric models (e.g., ARMA, ARIMA, GARCH, EGARCH, GJR) or machine learning algorithms.

- Interface to DSGE models to forecast key economic variables.

- Use functions for interest rate modeling and forecasting based on parameters estimated from the Nelson-Siegel or Svensson models.

Explore Products

Derivatives Pricing

- Calculate price and greek variables of exotic options using Monte Carlo simulation in MATLAB significantly faster than running them in Visual Basic, R, and Python.

- Choose various pricing methods (e.g., closed-form equations, binomial trees, trinomial trees, and the stochastic volatility model) to price options. These include European options, American options, Asian options, barrier options, caps, floors, swaps, and multi-underlying asset derivatives.

- Run compute-intensive applications in parallel or deploy them to a GPU.

- Interface with Numerix.

Explore Products

Insurance and Actuarial Science

- Analyze large data sets, create custom actuarial models, and easily accelerate the simulations using parallelization.

- Build custom risk models using MATLABas a platform for Solvency II.

- Price various insurance products such as variable annuities, guaranteed minimum benefit options, term assurance, and endowment policies.

Explore Customer Success Stories:

Explore Products

Get a Free Trial

30 days of exploration at your fingertips.

Free eBook

Modeling Financial Risk with MATLAB